Quality vs. Quantity: Financial Reporting for Elected Officials

E-Quarterly Newsletter - September 2025

– By Kyle Sawyer, Director of Fiscal Consulting,

KateLynn Harrigan, Senior Fiscal Consultant,

Randy Anderson, School Finance Product Manager,

and Brian Reilly, Senior Municipal Advisor | Managing Director

Focus on Quality & Timeliness When Reporting to Elected Officials

As decision makers for and stewards of governmental jurisdictions, elected officials need timely, concise, and understandable financial information to guide their judgement when evaluating choices that can have long-lasting impacts. Finance staff are tasked with providing this information to a disparate group of individuals that may not have foundational knowledge of government finance, capital planning, and other fiscal matters.

Furthermore, while there are best practices in financial reporting, different approaches can be established that meet the needs of your entity. Factors such as size and complexity, number of funds and their types, and specific characteristics of your organization should inform how staff engage with elected (and appointed in some cases) officials on financial matters, including what data is relevant and how frequently reporting occurs.

Importantly, staff must recognize that establishing the annual budget and presenting the audited financial statements are only pieces of a larger puzzle. The question is: are there 20 pieces or 100? Staff must also have a motivation for education and context, while being transparent with elected leaders and the public. Both too much and not enough information can foster an environment of confusion and even skepticism. The focus should be on quality and timeliness, set against the backdrop of what’s important for your organization. And, if you find something isn’t working or might be better, you can always shift gears along the way.

Municipalities – General Fund

All municipalities have a General Fund that serves as their main operating fund, accounting for revenues and expenses to support core services such as public safety, administration, and public works. Information on how core services are provided, how much they cost, and how they are funded are critical for elected officials to understand and make informed decisions. The task of determining the level of detail and frequency of reporting that needs to occur is up to finance staff in consultation with elected officials.

There are annual requirements for reporting on the audit and preparing a budget, but that shouldn’t be the minimum. Finance staff should consider the size and complexity of the municipality along with the knowledge base of elected officials when determining frequency of reporting and level of detail provided. Beyond the prescribed annual reporting, it is best practice to report information quarterly or monthly, with more complex municipalities utilizing the latter. More important than the frequency is the timeliness and accuracy of the reporting and striking a balance between timeliness and reliability. Information should be reported as soon as it is reliable after the end of the designated period to ensure elected officials have an opportunity to weigh in on factors such as service delivery, program outcomes, and financial health.

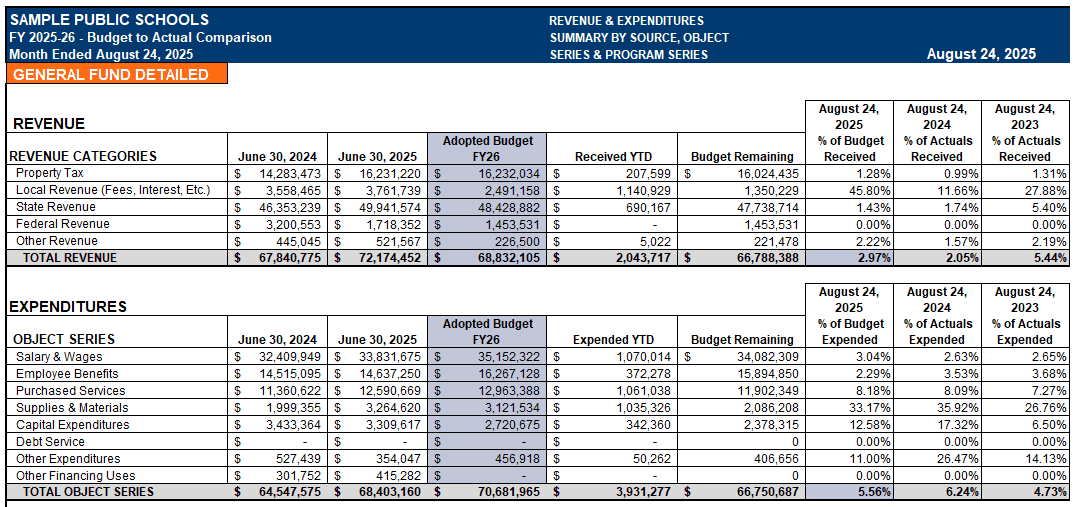

Actual results should be compared to budgeted amounts and presenting line-item details should be avoided. Summary level information should be the focus and is best provided at a category (personnel services, professional services, taxes, charges for services, etc.) and/or department level (police, fire, parks, and recreation, etc.). Finance staff should be prepared to answer summary level questions with detailed line-item responses for an efficient and effective reporting process. For example, if professional services are over budget, staff should be prepared to explain that engineering and legal fees are up because of an ongoing project or event rather than having elected officials spend time looking at and questioning the engineering and legal fees line items in a voluminous report. Another important factor to consider is not all months (or periods) are the same and the budget is typically not broken out by month. A good example of this on the revenue side is property taxes which are received in multiple installments during the year rather than monthly. To help explain the ebbs and flows of a given year it is important to also present year-over-year information and trends to show annual alignment or material variances.

Financial position metrics can also be a useful tool for elected officials to understand the immediate financial resources available and how they compare to their peer municipalities. For example, calculating the percentage of General Fund Unrestricted Fund Balance to budgeted expenditures indicates the ability of the municipality to maintain services during an economic downturn or unforeseen event. When comparing to peers, revenue (or expense) per capita provides insight into financial capacity and trends relative to the size of the municipality against comparable jurisdictions.

Effective General Fund financial reporting is critical to the success of both the finance staff and elected officials. Elected officials remain informed, can make strategic decisions, and be transparent with constituents while staff receive regular feedback that helps inform current spending priorities and future projects, initiatives, and budgets. Managing the General Fund is a team effort, and when reporting and communication are done well everyone benefits!

Municipalities – Enterprise Funds

Another common fund type for many jurisdictions is called proprietary funds. Proprietary funds recognize the assets, liabilities, revenues, and expenses of business-like activities overseen by the community. Proprietary funds are meant to be self-sustaining and not supported by the general tax levy. The most common type of proprietary funds are the enterprise funds that provide services to the public, such as utilities. The expenses of enterprise funds are mainly supported through user fees and charges.

Communities should consider reporting for enterprise funds on a similar schedule as revenues of the fund are administered. The most common schedules for billing are done on a monthly or quarterly basis. Comparing month-to-date, or quarter-to-date reports against prior-year same period reports can help ensure billing is accurate and catch any discrepancies quickly.

Year-end fund review is important as well. Enterprise funds are meant to be self-sustaining. A utility fund that is reporting year over year deficits means that user fees are no longer supporting expenses and a fee increase may be worth pursuing. Fee increases should take into consideration several years of historical data as well as current and future year information if data is available. Revenues and expenses are rarely static and may fluctuate throughout the year. Reviewing a more robust set of data will help to balance out irregularities in revenues and expenses that can happen for various reasons such as new developments, construction projects, major repairs, and faulty equipment.

Before a fee increase is implemented it is a common practice to compare your utility fees and charges with communities in your county and/or state. While this information is important to consider, always remember utilities are designed to meet the unique needs of the residents, businesses, and institutions they serve. Those needs can significantly vary from one community to another, and fee structures often reflect the unique needs of that user base. Focus first on what is the best decision to make for the fiscal sustainability of the utility and second on the comparison of rates against surrounding community charges.

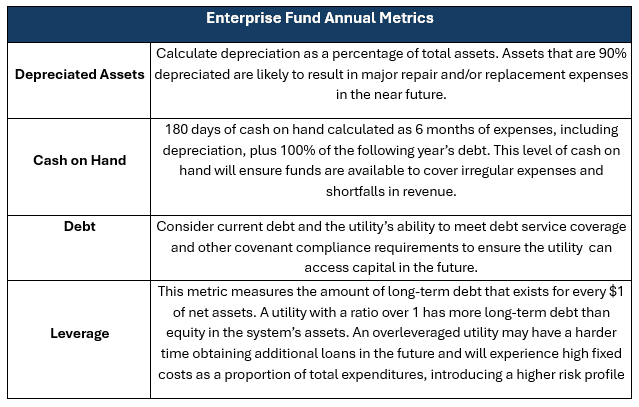

Some easy to review annual metrics to ensure fiscal sustainability include:

Calculating these metrics no less than annually and reporting to the utility’s elected or appointed body will help craft a path towards long-term financial success with less chance of “knee jerk” decision making.

Ignoring the age of assets, depleting a utility fund’s cash, and not ensuring revenues are meeting and/or exceeding expenses annually are the biggest ways to end up with large irregular fee increases for customers. Annual reviews can help avoid this problem.

School Districts

According to Minnesota statute, each Minnesota school district must adapt the uniform financial accounting and reporting standards (UFARS) for Minnesota school districts provided for in guidelines adopted by the Minnesota Department of Education (MDE).

Each school district is required to prepare audited financial statements annually and submit them to the Minnesota Department of Education Commissioner and Office of the State Auditor by December 31st. The audited financial statements must also provide a statement of assurance pertaining to uniform financial accounting and reporting standards compliance, as well as a copy of the management letter submitted to the district by its auditor.

Minnesota school districts are not required to provide mandatory monthly or quarterly public financial reports. Although not required, administrative staff usually report monthly or quarterly to the school board or a supporting group such as a finance committee. Many business services departments prepare monthly financial reports to monitor revenues, expenditures, and fund balances internally. These monthly exercises help district leaders manage finances and track progress against the annual budget. They also provide transparency for district stakeholders which helps to promote trust.

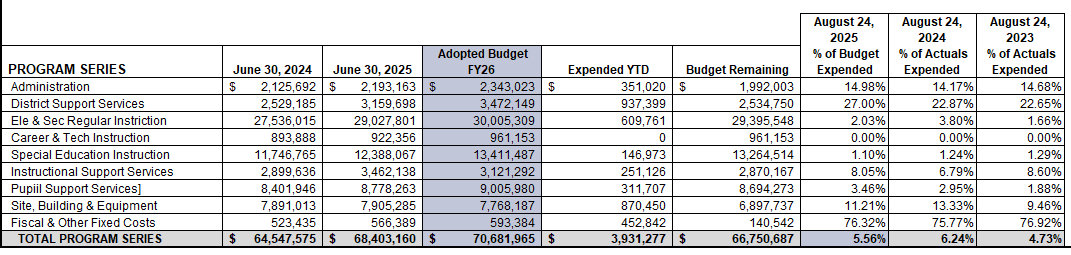

The reports used will normally be at the category level using revenue source categories and expense object and program categories. Metrics at the end of the month compare the percentage used for the current year compared to the previous years. This gives leaders a chance to analyze whether the current year budget is tracking as compared to previous years. It also helps to solve problems if some of the categories are not in line with what was previously spent or received.

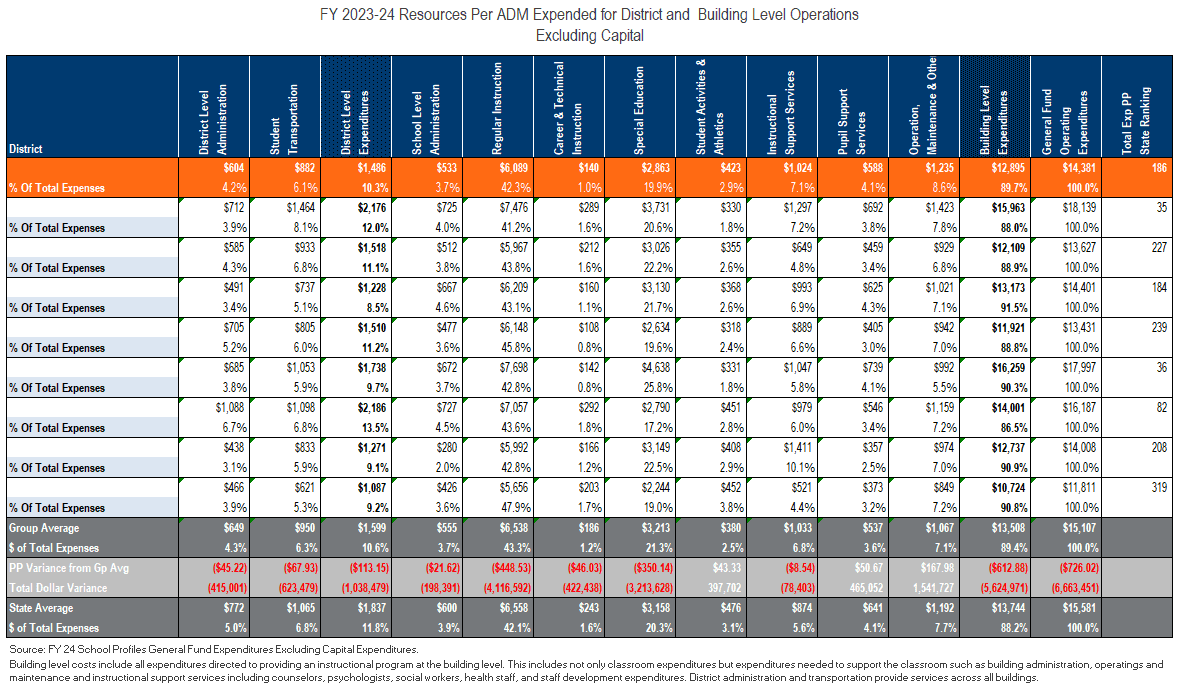

School district business leaders will also use certain benchmarks when comparing data with other school districts. The main benchmark is on a per pupil basis or adjusted daily membership (ADM). This gives business leaders the ability to see how their school district traits compare to other schools against the state average and whether any adjustments need to be made.

Business leaders have several tools that they can use to monitor the performance of the school district. These can be in the form of mandatory reports that need to be submitted on an annual basis. Monthly/quarterly reports that oversee how the school district is performing on a budget versus actual basis. Comparing districts to see if what your district spends/receives is in line with similar districts.

Monitoring your school district’s performance is of the utmost importance in the financial management of a school district. It helps to match initiatives and the strategic plan with financial resources. It also promotes transparency, accountability, and trust.

All Jurisdictions – Debt & Liabilities

While debt is a four-letter word, it’s not a dirty one. Debt is an important tool that, when used appropriately, can provide for generational investments, a healthy capital stock, and well-functioning infrastructure. When used without proper planning and foundational knowledge, debt can lead to budgetary pressures and an inability to invest in critical resources.

As with other financial measures, there is no one-size-fits-all framework to gauge a comfortable amount of debt. While some states place explicit limitations on things like general obligation debt, some do not or provide a wide array of exceptions from limits. Where there are limitations, it’s wise to stay current with where your jurisdiction measures up in this regard. The general rule of thumb is to always retain at least 10% – 20% of statutory capacity in reserve, depending on the size of your jurisdiction. For smaller communities, it’s better to focus on a dollar limitation (e.g., $1 million) instead as percentages, as percentages in the range above can result in nominal dollar amounts that are insufficient in the event of an emergency or opportunity.

Additionally, when reviewing general obligation debt metrics, it’s important to categorize and net out G.O. debt that is supported from revenues other than generally applicable taxes. As an example, many communities might issue G.O. debt for utility improvements and use the enterprise fund’s revenues to support the required debt payments and abate the required levy. Leases obligations supported by generally applicable property taxes should also be included in this figure, even though payments are typically subject to annual appropriation.

Some common benchmarks and ratios for tax-supported general obligation debt that can be reviewed annually include:

- Debt per capita

- Debt as a percentage of total market value

- The percentage of the general fund budget comprised of debt service (should be no greater than 25%)

When evaluating total general obligation debt (paid from all sources), finance staff should also present how many years until 50% of the principal outstanding is retired, with 10 years and less being viewed favorably.

With respect to revenue-secured obligations, it is important to annually review the debt service coverage ratio. Most utility revenue obligations are secured by a pledge of “net” revenues. Net revenues are defined as operating revenues fewer operating costs, excluding interest, adding back depreciation, and including the net amount of non-operating revenues/expenses. This number is then measured against annual debt service or maximum annual debt service (for all debt secured by the pledge) to arrive at ratio often referred to as debt service coverage. A typical covenant for revenue debt is to maintain a minimum debt service coverage ratio (DSCR) of 125%.

When including both revenue and general obligation debt in the calculation, the DSCR should get no lower than 110%. When below this threshold, the enterprise is likely not generating sufficient cash flow to pay for capital costs, such as repairs and improvements to the system.

All Jurisdictions – Cash & Investment Reporting

Like general and enterprise fund reporting, providing information related to cash and investments should be tailored to the characteristics and complexities of your jurisdiction.

When it comes to cash, monthly reporting is generally the best approach, which aligns with monthly cash reconciliations and disbursements. To the greatest degree possible, cash balances should be monitored by fund, even if a jurisdiction maintains a comingled back account. Perfection isn’t the objective. Rather, there needs to be insight across all funds to ensure that one (or more) respective fund isn’t “borrowing” from another over the course of a fiscal period. When interfund borrowing for cash flow purposes is presenting itself persistently, this is likely a sign of stress that could result in drawing down cash in the aggregate when not addressed. No entity has an unlimited supply of cash. If cash balances are consistently declining year-over-year without a conscious decision to do so, investigation is warranted to remedy the problem.

Reporting related investments can present a more complex mosaic. For some jurisdictions, annual reporting might be sufficient. In many others, quarterly reporting of specific information is reasonable, with a broader update on an annual basis once the fiscal period is closed out.

Investments are most commonly reported on a mark-to-market basis, meaning changes in market value are taken into consideration when reviewing balances. However, most fixed-income investments are held to maturity, which means those changes in market value might just become “noise” to the average person. That isn’t to say those measures should be excluded but perhaps supplemented with other metrics like book value. Book value is an accounting metric that views investments through the lens of how individual investment positions move along the spectrum of purchase price to maturity value.

Presenting summary level or individual holdings detail should be considered in the context of the size of the portfolio. It’s unrealistic for elected officials to digest information associated with a portfolio of dozens of individual securities on regular intervals throughout the year. However, that information should likely be presented at least annually.

Summary level metrics can be reviewed more frequently and should include:

- Measures of portfolio diversity, such as percentage mix of asset types (i.e., US Treasuries, agencies, CDs, municipals, etc.)

- The weighted average maturity of the portfolio

- The weighted average credit quality of the portfolio

- Balances held in each account or with one or more custodians

- Changes in market value during the period

- Income recognized over the period, year-to-date, and forecasted out through the remainder of the fiscal year

If external investment managers are used, those parties should report to the committee overseeing the investment function or the governing body no less than annually. Commentaries or other summary reports can be provided more frequently, if desired.

Summary

The importance of providing elected officials and the public with clear, concise, and timely financial reporting is critical to fostering an environment of transparency, which establishes trust and confidence within your jurisdiction and among its constituents.

Through regular reporting, staff and the governing body are more prepared to make decisions judiciously and hopefully with little controversy. When elected leaders are informed, annual events like budgeting become far more efficient and through the lens of long-term financial stewardship.

Beyond your own borders, strong financial reporting and planning is viewed favorably by outside parties like rating agencies and investors. A demonstrated track record of a rigorous reporting regimen can truly bring economic benefits beyond what is obvious to those around you.

Ehlers’ team of advisors and consultants can partner with you to establish a reporting program tailored to your specific needs. We’d love to hear from you.

Required Disclosures: Please Read

Ehlers is the joint marketing name of the following affiliated businesses (collectively, the “Affiliates”): Ehlers & Associates, Inc. (“EA”), a municipal advisor registered with the Municipal Securities Rulemaking Board (“MSRB”) and the Securities and Exchange Commission (“SEC”); Ehlers Investment Partners, LLC (“EIP”), an investment adviser registered with the SEC; and Bond Trust Services Corporation (“BTS”), holder of a limited banking charter issued by the State of Minnesota.

This communication does not constitute an offer or solicitation for the purchase or sale of any investment (including without limitation, any municipal financial product, municipal security, or other security) or agreement with respect to any investment strategy or program. This communication is offered without charge to clients, friends, and prospective clients of the Affiliates as a source of general information about the services Ehlers provides. This communication is neither advice nor a recommendation by any Affiliate to any person with respect to any municipal financial product, municipal security, or other security, as such terms are defined pursuant to Section 15B of the Exchange Act of 1934 and rules of the MSRB. This communication does not constitute investment advice by any Affiliate that purports to meet the objectives or needs of any person pursuant to the Investment Advisers Act of 1940 or applicable state law. In providing this information, The Affiliates are not acting as an advisor to you and do not owe you a fiduciary duty pursuant to Section 15B of the Securities Exchange Act of 1934. You should discuss the information contained herein with any and all internal or external advisors and experts you deem appropriate before acting on the information.